|

Issue No. 012 · Mon, May 18, 2026

|

● Daily Brief

|

|

|

Decision Layer

|

Finance

· 5 min read

|

|

| YS |

From Yatharth Sejpal · CEO, KNOWIDEA |

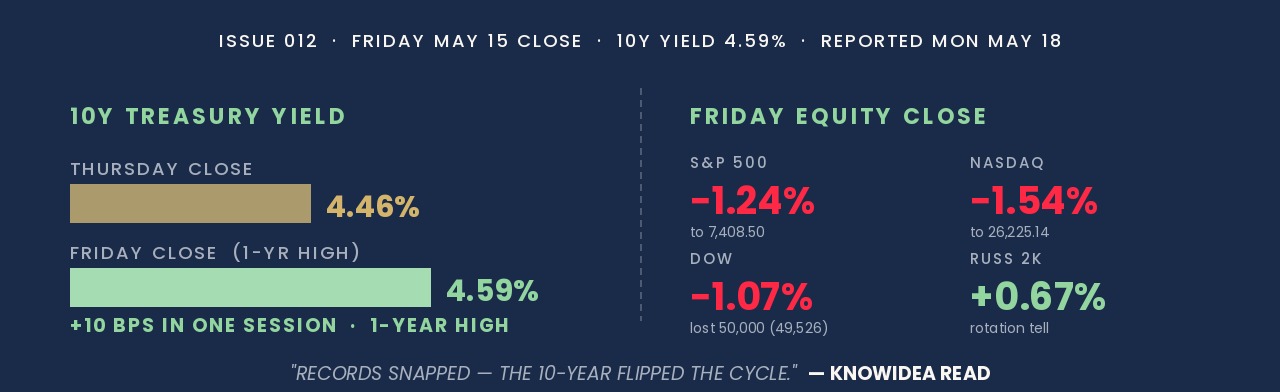

Friday delivered the regime shift the bulls had been refusing to price. The 10-year Treasury yield closed at 4.59 percent — its highest level since February 2025 — with the 2-year at 4.09 percent. The yield spike, driven by Iran-war inflation pass-through and a hawkish read on the incoming Warsh Fed, finally broke the AI-led rally. The S&P 500 fell 1.24 percent to 7,408.50. The Nasdaq dropped 1.54 percent to 26,225.14. The Dow Jones lost 537 points (-1.07 percent) to 49,526.17 — surrendering the 50,000 mark it had just reclaimed Thursday. Semiconductors led the retreat: Intel -6.7 percent, Micron -6.6 percent, AMD -5.7 percent, Nvidia -4.4 percent, Marvell -5 percent. Cerebras Systems (CBRS) gave back 10 percent of its 68 percent IPO-day gain. CME FedWatch now puts the odds of a 2026 Fed rate hike at 45 percent — up from 1 percent a month ago.

Underneath the tape, the structural news was Berkshire Hathaway's Q1 13F — the first under CEO Greg Abel, filed Friday. Berkshire exited Amazon, Visa, Mastercard, UnitedHealth, Domino's, Aon, and Heico entirely, took a new $2.65 billion stake in Delta Air Lines, established a $1 billion position in Alphabet Class C while tripling its Class A holding to roughly $15 billion, and trimmed Chevron materially. The portfolio shrank from $274 billion to $263 billion and from 40 holdings to 26; cash sits at a record $397 billion. The Empire State Manufacturing Index also surprised, jumping to 19.6 — its highest reading since April 2022 — against a 7.8 consensus, with prices-paid hitting 62.6. Inside, we unpack why the rate-hike repricing is the dominant signal, how to read Abel's first portfolio under his name, and what the 4.59 percent 10-year means for the AI trade through the rest of Q2.

|

10-year hits 4.59%. Dow loses 50,000. Fed odds flip from cut to hike.

The session reads like a single coordinated repricing. Records on Thursday, then 1-to-1.5 percent declines across all three indexes Friday as the 10-year vaulted to a one-year high and the rate-hike trade went mainstream. Berkshire Hathaway’s Q1 13F — Greg Abel’s first as CEO, filed at the bell — confirmed the rotation: out of financial-payment names, out of mega-cap retail, into airlines and Alphabet. The Empire State print of 19.6 is bullish on activity but inflationary on inputs — the very combination that just blew up the rally.

Friday Close · 10Y Yield 4.59% Highest Since Feb 2025 · Friday, May 15, 2026

The yield move was the trigger. The 10-year Treasury yield jumped nearly 10 basis points to close at 4.59 percent, its highest level since February 2025; the 2-year ended at 4.09 percent, also a multi-month high. The catalyst was a one-week succession of inflation prints — CPI and PPI hot, import prices up 4.2 percent year-over-year, and Friday’s Empire State Manufacturing Index jumping nine points to 19.6 against a 7.8 consensus with prices-paid climbing twelve points to 62.6. The bond market read every line through the lens of the same question: under Warsh, does the Fed lean on the new energy-driven inflation? CME FedWatch now puts the chance of a Fed rate hike in 2026 at roughly 45 percent — up from 1 percent one month ago. The S&P 500 fell 1.24 percent to 7,408.50; the Nasdaq dropped 1.54 percent to 26,225.14; the Dow lost 537 points (-1.07%) to 49,526.17, giving up the 50,000 line one session after reclaiming it.

The selling was concentrated where the rally had been most stretched. Intel fell 6.7 percent, Micron 6.6 percent, AMD 5.7 percent, Marvell 5 percent, ARM and ASML 4 percent each, and Nvidia 4.4 percent ahead of its earnings print on Wednesday. Cerebras Systems (CBRS), which had surged 68 percent in its Nasdaq debut Thursday after raising $5.55 billion in the largest US tech IPO since Uber 2019, gave back 10 percent. The Russell 2000 was the outlier, gaining 0.67 percent — the rotation signal under the headline indexes. The clearest institutional read came from Berkshire Hathaway’s Q1 13F filed Friday, Greg Abel’s first as CEO: complete exits from Amazon, Visa, Mastercard, UnitedHealth, Domino’s, Aon, Pool, Heico, and Formula One; a new $2.65 billion stake in Delta Air Lines; a new $1 billion Alphabet Class C position with the Class A holding tripled to roughly $15 billion; a small Macy’s position; and a material trim to Chevron. The 13F portfolio shrank from $274 billion to $263 billion and from 40 names to 26. Cash sits at a record $397 billion.

The cross-asset confirmation was uniform. Gold fell 2 percent to $4,556.46 — a more than one-week low — as rising real yields and a stronger dollar removed the bid; the dollar index posted its best weekly gain in two months. WTI crude added 4.2 percent to close near $106 and was up 11 percent on the week as the Strait of Hormuz stayed effectively closed. The Trump-Xi summit concluded in Beijing with no breakthrough on Iran, no firm Hormuz commitment in Chinese state media, and a confirmed Boeing 200-jet order (smaller than the 500-jet, $77 billion deal markets had been positioned for); Boeing fell 2.8 percent to $222.70. Dan Niles, founder of Niles Investment Management, told CNBC 10 of the last 12 recessions were preceded by an oil-price spike and that “this is starting to get uncomfortable.” Jerome Powell’s term as chair ended at the close. The Fed Board named him chair pro tempore pending the swearing-in of Kevin Warsh, who has been a public critic of the Fed’s balance sheet and has called for “regime change” at the central bank. His first FOMC meeting is June 16-17.

|

4.59%

10-Year yield (highest since Feb ‘25)

|

49,526

Dow close (back below 50K, -537 pts)

|

|

$397B

Berkshire Q1 cash (record)

|

45%

2026 rate-hike odds (vs 1% a month ago)

|

|

Three angles, depending on where your money sits.

|

If you have a mortgage, an HELOC, or are house-shopping

Friday’s 10-basis-point spike in the 10-year to 4.59 percent flows directly into 30-year mortgage rates within 1-2 weeks. If you’ve been waiting for a rate-cut window to refinance, that window just narrowed materially — Fed-rate-hike odds for 2026 jumped from 1 percent to 45 percent in a single month. Lock any pending HELOC or floating-rate exposure to fixed now if you can; the carry math has changed. For house-shoppers, the 30-year mortgage rate is likely heading into the high 7s on this re-pricing. Don’t assume the AI-driven equity rally protects your housing budget — the same inflation pushing yields up is what flipped the Fed. Build a budget assuming rates stay elevated through Q3 2026 minimum.

|

|

|

If you sit on a finance team or treasury desk

Berkshire’s clean exit from Visa, Mastercard, Amazon, and UnitedHealth is the most consequential capital-allocation signal of the quarter. Greg Abel is concentrating the book and stockpiling cash at $397 billion — not deploying into the AI mega-caps. That is a deliberate read on duration risk, valuation, and where the next decade’s incremental returns sit. Mirror the discipline: stress-test your debt portfolio for a 50bp yield spike from here (10-year hitting 5.10%), trim duration in any rate-sensitive corporate-debt sleeve, and pull forward any refinancing or term-out conversations to the next two weeks. If your firm holds floating-rate revolvers, model a 75bp hike scenario and the resulting EBITDA-to-interest coverage compression now — before the next FOMC.

|

|

|

If you allocate capital or watch the Fed

The trade has shifted from cut-pricing to hike-pricing in 30 days — that is a regime change, not a wobble. Underweight long-duration tech, overweight the Russell 2000 cohort that gained 0.67 percent into Friday’s selloff, and add quality-cyclical industrials that Abel’s 13F just validated (Delta is the marquee). The Russell’s outperformance into broad weakness is the rotation tell: small-cap cyclicals reprice on domestic activity (Empire State 19.6) before the macro fully turns. The pair: short the AI-mega-cap basket where 2026 P/E multiples assume rate cuts that are no longer in the price. Warsh’s first FOMC is June 16-17 — position before the dot-plot release that prints with it.

|

|

|

Four other moves from Friday that all pointed the same direction.

|

|

Berkshire’s first 13F under Abel: exits Amazon, Visa, Mastercard; triples Alphabet.

Berkshire Hathaway’s Q1 13F filing — the first under CEO Greg Abel — disclosed complete exits from Amazon, Visa, Mastercard, UnitedHealth, Domino’s, Aon, Pool, Heico, and Formula One, alongside a new $2.65 billion Delta Air Lines stake, a new $1 billion Alphabet Class C position, a tripling of Alphabet Class A to roughly $15 billion, and a small Macy’s stake. Chevron was cut materially. The 13F portfolio shrank from $274 billion to $263 billion, holdings from 40 to 26, and cash reached a record $397.38 billion. Buybacks of roughly $234 million resumed. The portfolio reads as a sector rotation, not a vote on the index.

|

|

|

Cerebras (CBRS) gives back 10% one day after 68% IPO surge.

Cerebras Systems — which jumped 68 percent on Thursday in its Nasdaq debut, the largest US tech IPO since Uber 2019 at $5.55 billion raised and a roughly $95 billion peak market cap — gave back 10 percent on Friday alongside the broader semiconductor cohort. Intel fell 6.7 percent, Micron 6.6 percent, AMD 5.7 percent, Marvell 5 percent, Nvidia 4.4 percent ahead of next Wednesday’s print. The IPO market is open for AI hardware; the multiple-expansion trade is not. Treat the gap-down as the first re-rating in the SOX premium, not a stock-specific event.

|

|

|

Empire State Manufacturing prints 19.6 — nearly 3x consensus.

The May Empire State Manufacturing Index jumped nine points to 19.6 from 11.0 in April — its highest reading since April 2022 — against a 7.8 consensus. New orders climbed to 22.7, shipments held at 18.9, and the future-business-conditions index rose 14 points to 33.5 with over 50 percent of respondents expecting improvement. The price components are the real story: prices-paid jumped 12 points to 62.6 and prices-received climbed 10 points to 31.8, both highest since 2022. Industrial production for April also beat at +0.7 percent versus +0.2 percent expected. The activity print is bullish, the price prints are why yields ripped.

|

|

|

Boeing -2.8% as China order undershoots the headline number.

Trump said Friday that China has agreed to purchase 200 Boeing aircraft equipped with GE Aerospace engines, with potential for up to 750 planes over time. The Street had positioned for a 500-plane, ~$77 billion deal — the initial 200 was therefore read as a disappointment, and Boeing shares fell 2.8 percent to $222.70. The Trump-Xi summit produced no concrete plan to reopen the Strait of Hormuz, no breakthrough on Iran, no Hormuz mention in Xinhua’s readout, and no nuclear-chip clarity (Trump said Nvidia chip sales to China did not come up). The summit is the cleanest reminder that announcement-driven trades require execution to clear.

|

|

|

◆ Bluff Check

Where today’s loudest narrative meets the data.

Markets are noisy. Executives talk their book. Press releases bury the lead. Each day we surface one prominent claim from the tape — a CEO quote, a research note, an official statement — and check it against the data. If the numbers back it up, we call it REAL. If the framing is doing more work than the evidence, we call it BLUFF. No drama, no theatrics — just the read.

| |

“We made some fantastic trade deals. A lot of different problems had been resolved.”

— President Trump, departing Beijing, Friday May 15

Our Read

The framing is that the two-day summit cleared the path on trade, Hormuz, AI exports, and Boeing. The data argues otherwise. The Boeing announcement disclosed 200 jets — below the 500-plane, $77 billion deal the Street had been positioned for; Boeing fell 2.8 percent. Xinhua’s Chinese-language readout made no mention of the Strait of Hormuz commitment or oil purchases. Trump separately told reporters the topic of Nvidia’s chip sales to China “didn’t arise” with Xi — the issue the chip cohort had been positioned to clear. No formal joint communiqué was published. The 10-year Treasury yield ripped to a one-year high of 4.59 percent on the same session; the S&P fell 1.24 percent; the Dow lost 50,000. If “a lot of different problems had been resolved,” the cross-asset tape would have rallied, not sold off in unison. The verdict reads from price.

|

|

|

◆ The KNOWIDEA Lens

Here’s how we’re reading the rate-regime flip.

Our Predictive Intelligence Engine ran Friday’s signals — the 10-year spike to 4.59 percent, the Dow loss of 50,000, Berkshire’s first 13F under Abel, the Empire State jump to 19.6 with prices-paid at 62.6, and the Trump-Xi summit with no Hormuz breakthrough — through 5 active data streams. Here’s what it surfaced.

| |

|

◆ Predictive Insight

Long-duration AI mega-cap names with 2026 P/E above the SOX median face 73% probability of 8–15% underperformance vs the Russell 2000 over the next 45 days — driven by the 10-year repricing from 4.46% to 4.59% in a single session and the Fed’s 2026 rate-hike odds jumping from 1% to 45% in 30 days, the Empire State prices-paid sub-index at 62.6 confirming inflation persistence into Warsh’s first FOMC on June 16-17, and Berkshire’s 13F validating the rotation away from rate-sensitive long-duration names toward industrial cyclicals like Delta. Cerebras’ 10% give-back is the early SOX premium re-rating signal.

|

Confidence

73%

|

Downside Risk

Medium-High

|

Horizon

45 days

|

|

What we'd do today →

|

1

|

Rotate into the Russell 2000 cyclicals that traded green into Friday’s rout. The R2K’s +0.67 percent gain against -1.24 percent S&P 500 is the cleanest rotation tell. Concentrate the long book in domestic-revenue industrials and quality cyclicals (the Berkshire-Delta validation tells you airlines specifically are now on the institutional bid). Equal-weight, hold for 45 days through the Warsh dot-plot. Trim long-duration AI mega-caps that have multiples assuming the rate cuts that just got repriced out.

|

|

2

|

Pre-position for the Warsh dot-plot before June 16-17. The market has moved from full rate-cut pricing to 45 percent hike-pricing in 30 days — an asymmetric move that still has room to extend. Buy short-dated TLT put spreads or long short-rate-curve trades to play one more leg higher in yields if PCE prints hot. Cap risk at 1.5 percent of equity; the trade unwinds quickly if Iran de-escalates or oil rolls over. Pair against quality industrials so the macro hedge does not become the only position you own.

|

|

3

|

Watch Nvidia’s print Wednesday for the rotation confirmation. Street consensus for Q1 is roughly $43-44 billion of revenue with Q2 guide above $48 billion expected; the multiple is now under pressure with the SOX off Friday and the China-chip-sales clarity that Trump confirmed did not come up at Beijing. Set tactical positions before the print: size NVDA exposure at ~2-3 percent of equity going in, with a put-spread collar to cap downside. If the print confirms but the stock fades, that is the genuine top tick for the AI-mega-cap cohort; rotate the proceeds into the Russell 2000 cyclical basket the same week.

|

|

|

◆ Want this on your portfolio?

30 minutes. The complete read on your positions.

We apply Friday’s signals to your specific portfolio — positions, treasury, hedge book — and walk through what P.I.E. recommends for you. No pitch. If we’re not a fit, we’ll tell you in the first 5 minutes.

|

|

Powered by the P.I.E. · Predictive Intelligence Engine

FUSE

›

SCAN

›

POSITION

›

CONVERT

›

PREDICT

›

DISTILL

›

DECIDE

|

|

KNOWIDEA

Predictive Intelligence Engine

© 2026 KNOWIDEA Technologies Ltd. · SOC 2 Verified

|

|